Housing is as hot a topic as ever.

The airwaves are filled with stories of bidding wars for single-family homes, skyrocketing rents, supply chain bottlenecks, and rising interest rates and inflation.

But have you ever wondered why all this is happening? While at first glance it may all seem disconnected, there’s actually a cohesive story to it all. And while the pandemic certainly played a major role, the story begins in the aftermath of the 2008 global financial crisis.

This article breaks down the state of the housing market, what it means for your business, and whether technology can make a difference in your operations.

The single-family home shortage

When the housing bubble burst around 2008, many homebuilders went out of business. The market bottomed in 2012, and Americans started buying homes again. The problem, however, was that single-family home construction did not pick up with demand, and the slump continued for over a decade. Meanwhile, millennials (the largest generation) started to settle down and buy houses. Skilled construction workers and tradespeople found new jobs in other industries, and combined with a shortage of less-skilled workers, a severe housing shortage developed — acutely felt among those looking for starter homes. Speaking to Globest.com, Al Lord, Founder and CEO of Lexerd Capital Management, explains:

“The construction industry cannot build fast enough to accommodate demand and does not build the ‘right’ units in large numbers, as the shortage is severe for starter family units and units below 1,400 square feet. The millennial generation, now 20% of the population, is ready to start forming families, but starter units are not available.”

So how much of a housing deficit is there?

It’s hard to say, exactly.

Freddie Mac research puts the number at 3.8 million units, while a 2021 report sponsored by the National Association of Realtors found there to be a supply gap of 6.8 million units. Whatever the number is, there is clearly a housing shortage that is growing more and more difficult to fill due to the following:

- labor shortages causing an increase in the cost of labor

- the cost of materials increasing over 30% since the start of the pandemic

- supply chain issues delaying project completions

- a lack of developed land

All of which has led to:

Skyrocketing home prices

Realtor.com data shows the median listing price in April 2022 was $425,000, up 14.2% from last year and up 32.4% compared to April 2020. According to the Federal Housing Financing Agency’s House Price Index, home prices rose 19.4% between February 2021 and February 2022. That is in line with the S&P CoreLogic Case-Shiller US National Home Price Index that puts the one-year increase at 19.8%.

So not only is the average American being priced out, they are also contending with:

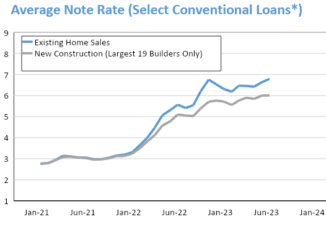

A sharp rise in interest rates by the Federal Reserve in an effort to curb rising inflation

The combination of the Federal Reserve “flooding the system with money” to rescue crashing financial markets in March-April 2020, supply chain issues, and a return to pre-pandemic demand for goods and services is causing inflation to reach highs not seen in 40 years. Indeed, in an AppFolio survey of over 1,000 property management companies, many of the top challenges cited were all inflation related (rising material costs, reducing overhead, navigating inflationary pressures, etc.).

Now, it’s on the Fed to taper down these levels by raising interest rates. Here’s the dynamic:

Higher interest rates make borrowing money costlier and less appealing, allowing demand to slow down and catch up with depressed supply. In theory, less demand will place downward price pressure on sellers (of whatever the product may be) to entice purchases.

And the strategy may be starting to work. The Consumer Price Index increased 0.3% in April after rising 1.2% in March. While this doesn’t necessarily mean that prices will begin falling, it could mean that inflation has peaked and prices have either plateaued or will rise at a slower rate. A Redfin analysis shows the typical buyer’s monthly mortgage payment has increased 42% year-over-year, the biggest annual gain on record. As a result, “the share of home sellers who dropped their asking price shot up to a six-month high of 15% for the four weeks ending May 1, up from 9% a year earlier. The 5.9% increase is the largest annual gain on record in Redfin’s weekly housing data back through 2015.” Demand for mortgages is at a two-year low, according to a Fannie Mae survey.

But houses are still unaffordable.

Analyzing data from Black Knight, Business Insider reports the monthly payment on a 30-year mortgage for an average-priced home with a 20% down payment now adds up to 31% of the median American household’s income. Freddie Mac weekly averages have increased 17 basis points since the time that article was published. In a Twitter thread, Rick Palacios Jr., Director of Research at John Burns Real Estate Consulting, shows how historically elevated prices and rising interest rates are shrinking the pool of buyers. He quotes homebuilders from across the country. For example:

- Houston builder: “Many first-time buyers simply no longer qualify with the increase in interest rates, as their debt-to-income ratio gets out of whack.”

- Seattle builder: “There has been a pause by a large population of buyers. To achieve our desired [sales] pace, we had to make price adjustments. Rates are starting to knock people out of qualification.”

- Philadelphia builder: “Between higher interest rates and higher sales prices, along with high gas prices and a volatile stock market, we’re seeing a pullback in our sales.”

At the moment, homeownership is unfortunately out of reach for most of the younger generations. There’s also another complication:

Rents have risen dramatically as well

While rent increases of 12 to 20% in suburban Philadelphia fall in line with ApartmentList.com’s analysis of year-over-year rent growth at 16.3%, rent increases are even higher in “hotter” markets. The Wall Street Journal reports how 58% increases in the Miami area are driving natives out. Rural Lewis and Clark County, Montana, has seen increases of 36.5%.

What all this means for property management

The lack of single-family homes to buy, combined with a near-term shortage of new apartment completions, can ultimately lead to less move-outs/more retention. Despite rising prices, there is a significant delta between average monthly mortgage payments and a rent obligation. Analysts at Marcus & Millichap calculate it at $638.

To make a lasting impression on both residents and property owners, it’s more important than ever to double down on operational efficiencies and be proactive about retaining residents. Consider how to get ahead of renewal conversations and better understand resident plans and motivations. The AppFolio National Renter Motivations Report found that 30% of renters view responsiveness, flexibility, and technology as more important now than before the pandemic. So how can technology help give your residents what they want?

We’ll be covering that in-depth in part two of this series. Stay tuned!

Source: Appfolio.com