A second consecutive benign set of inflation prints adds to optimism that the Fed rate hike cycle is at an end and a soft landing is achievable for the US economy. We continue to have our concerns about the economic outlook, centred on the abrupt hard stop in credit growth, but the Fed will soon be in a position to be able to cut rates if a recession materialises

US inflation pressures continue to ease

The US consumer price inflation report showed that prices rose 0.2% month-on-month at both the headline and core (ex food and energy) level as was expected. To two decimal places it was even better at 0.17% and 0.16% respectively, which meant that the annual rate of headline inflation came in at 3.2% rather than 3.3% (versus 3% in June). Core inflation slowed to 4.7% from 4.8% as expected.

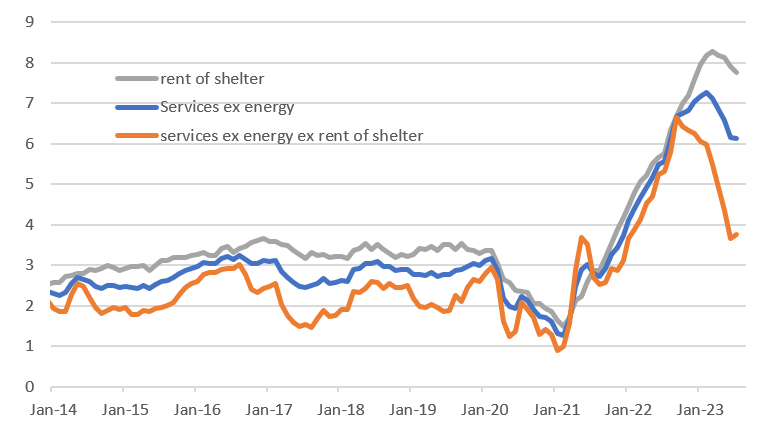

A decent drop in used car prices helped (-1.3% MoM), but a second consecutive large decline in air fares (-8.1%) is a bit of a surprise. With medical care (-0.2%), recreation (0.1%), education (0%) and other goods and services (0.1%) all very subdued the Federal Reserve has got to be pretty happy with this. That so-called ‘supercore’ services (services ex energy ex housing) looks like it comes in at around 0.2% MoM, although the year-on-year rate ticks higher a little due to base effects.

Supercore services on the right path (YoY%)

Housing costs rose more than we thought though, with owners’ equivalent rent (the largest CPI component with a 25% weighting) rising 0.5% MoM/7.7% YoY but all in this report supports the nice golidlocks scenario of a slowdown in inflation allowing the Fed to stop hiking and eventually cut rates next year, which catches the slowing economy in time to prevent a recession. Obviously a lot can go wrong and we think it probably will given the worries about the abrupt slowdown in credit growth, but for now this data is encouraging.

Loading…

Source: think.ing.com

ENB

Sandstone Group