Global equity markets jumped while gold dropped in the past week on growing hopes of a deal in Washington to raise the debt ceiling to avoid a catastrophic default. However, some of the optimism scaled back after reports on Friday that debt ceiling talks have hit a roadblock after a White House spokesperson said serious differences remain with Republicans.

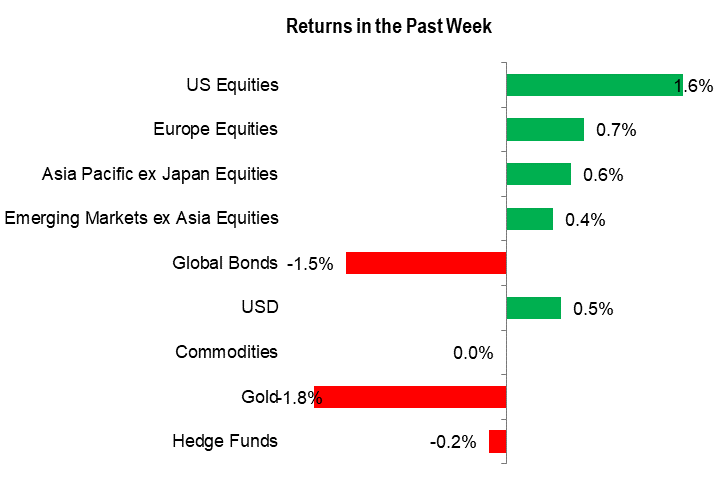

The S&P 500 rose 1.6%, while the Nasdaq 100 index surged 3.5%. The German DAX 40 advanced by 2.3% while the UK FTSE 100 was flat. In Asia, the Hang Seng index fell 0.9%, while Japan’s Nikkei 225 soared 5.0%. US Congressional Budget Office has said the US faces a “significant risk” of defaulting on payment obligations within the first two weeks of June without a debt ceiling increase.

Past week market performance

Source Data: Bloomberg; chart prepared in excel.

Note: Global Bonds proxy used is Bloomberg Global Aggregate Total Return Index UnhedgedUSD; Commodities proxy used is BBG Commodity Total Return; Hedge Funds proxy used is HFRX Global Hedge Fund Index.

Meanwhile, Fed Chair Powell left the door open for a pause at the June meeting. Tighter credit conditions mean that “our policy rate may not need to rise as much as it would have otherwise to achieve our goals,” Powell said on Friday. The central bank chair reiterated that the central bank would now make decisions “meeting by meeting”. The question for markets is if a pause means an end of the tightening cycle or a hold, highlighted by Atlanta Fed President Raphael Bostic earlier in the week. “I would say it was a pause, but a pause could be a ‘skip’, or it could be a hold,” Bostic said. Markets are currently pricing in a 45% chance of 75 basis points of rate cuts by the end of the year.

China/Hong Kong equities underperformed their peers after weaker-than-expected China data, including retail sales, industrial output, and fixed asset investment, on concerns that the post-Covid recovery is losing momentum. This follows the unexpected contraction in the manufacturing sector earlier in the month amid deepening producer price deflation. However, any stimulus measures to support the economy could cushion some of the downside risks, keeping the economy on an overall recovery trajectory for the entire year.

US debt ceiling talks are likely to dominate sentiment in the coming week. Furthermore, Fed speak is expected to continue through the coming week starting Monday; the Reserve Bank of New Zealand’s interest rate decision on Wednesday (expected to hike the benchmark rate by 25 basis points to 5.5%). Also, UK inflation data for April and Germany’s Ifo Business Climate are due on Wednesday. FOMC minutes, Germany Q1 GDP and Gfk Consumer Confidence, and US Q1 GDP are due on Thursday; Australia and UK retail sales for April, and US core PCE price index and durable goods data are due on Friday.

Source: www.dailyfx.com

ENB

Sandstone Group