This article is part of our 2022 – 2023 Housing Market Update series. After the series wraps, join us on February 6 for the HW+ Virtual 2023 Housing Market Update. Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the data for this year, along with a roundtable discussion on how these insights apply to your business. The event is exclusively for HW+ members, and you can go here to register.

We might only be a few weeks into 2023, but these first weeks have been rich with informative data. We’re already starting to see signals for what the market will look like this spring and beyond.

Mortgage Rates

In January, rates were hovering in the 6% range. Inflation and CPI have been leading to lower overall interest rates — specifically mortgage rates. Last fall, when mortgage rates first jumped over 7% we could see dramatic and immediate slowdown in buyer demand. Throughout January, as rates have drifted down closer to 6%, buyer activity has picked up quickly.

Our data shows that mortgage rates are going to be key this year. If economic conditions cause rates to jump over 7%, expect buyers to sit on the sidelines, allowing active inventory to build and time to sell a home to climb. On the other hand, if rates slide under 6%, we can already see that buyers are eager.

If you are working with first-time homebuyers or low-income borrowers, remind them of the abundance of programs available that reduce rates or support smaller down payments. Programs like these are great opportunities for first-time buyers to break into the market, even when mortgage rates are higher.

Inventory

In late January, there were 465,000 single family homes on the market, all across the country. That is 36% fewer properties for sale than the numbers we had prior to the pandemic, but still much higher than the inventory we had in early 2022.

We’re not seeing any indication that there will be a surge of new inventory anytime soon. Home sellers are listing very few homes right now, probably because they have very cheap mortgages, and any new home they move into will have significantly higher payments. As a result, inventory declined with few new listings and a surprising number of buyers. In 2023, inventory will likely be back to following the traditional, seasonal pattern that we were all used to prior to the pandemic, though the market will still have tighter supply than in those days.

Unlike the patterns we saw during the COVID-19 pandemic when homes were listed for sale and sold almost immediately, most homes listed for sale today will remain on the market for at least a few weeks. We can see evidence of multiple offers on homes in January, but these are coming in at around the asking price, rather than the over-bidding wars we saw during the pandemic.

I expect inventory to start climbing in earnest in February, peaking for the year in the late summer and ending 2023 with fewer than 700,000 homes on the market. Even though the patterns are more normal, inventory is still tight and will remain more restricted than some buyers might be hoping for.

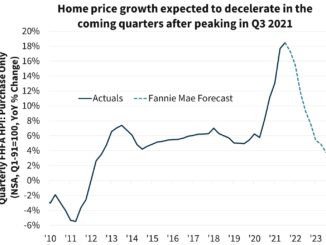

Pricing

In late January, the median price of single family homes in the U.S. was $414,900. This is slightly higher than the median from this point in 2022. But the pricing trend we are most interested in right now is the median price of new listings each week.

The median price of new listings is currently $379,900. In 2022, the new listing price was skyrocketing each week as sellers knew that buyers were bidding on everything very quickly. This January, demand is certainly weaker, but the data shows that supply is sufficiently tight and demand sufficiently strong to keep a floor on home prices. This indicator of price stability is a change from the very cold market of the third and fourth quarters of 2022, when demand was so weak, the price of the new listings was falling each week.

We can use levels of price reductions as a leading indicator of future sales prices. Currently, 33.9% of properties on the market have taken price reductions in 2023, and this number is dropping. While this is a bit higher than the usual 30% in typical years, it’s way lower than the 43% we saw in December. This is one data point illustrating a bit of a surprising turnaround in buyer demand.

From the data we’ve collected near the end of January, we can already see that home prices have stopped the pullback we saw in the second half of 2022. Unless mortgage rates spike above 7% consistently in the next few months, it seems unlikely that home prices will drop substantially in 2023 as some market prognosticators have written. We simply have too few sellers to satisfy the current demand levels.

On the other hand, there’s no indication in the data that home prices will climb substantially either. We see some home buyer demand, but we also see that buyers will stop abruptly as rates rise and affordability weakens. This is why we expect home prices in 2023 to finish the year in a similar space as the end of 2022.

This column does not necessarily reflect the opinion of HousingWire’s editorial department and its owners.

To contact the editor responsible for this story:

Sarah Wheeler at sarah@hwmedia.com